- → Why Your Health Insurance Ends When You Resign

- → What Dependent Status Means and Whether You Qualify

- → Who Can Register You as a Dependent

- → Documents You Need to Prepare Before You Start

- → Decision Flowchart: Which Path Is Right for You?

- → Step-by-Step: Registering on the NHIS Website

- → Coverage Options Compared

- → How to Confirm Your Coverage Is Active Online

- → What to Do If You Have No Eligible Family Member in Korea

- → Frequently Asked Questions

When you resign in Korea, your employer-sponsored health insurance ends almost immediately — often on the last day of the month. If you have a spouse or family member with active workplace insurance, registering as a 피부양자 (Pibuyangjja — dependent) keeps you fully covered at zero monthly cost. The critical window is 14 days from your last day of employment. Miss it, and your backdated coverage disappears. This post walks you through every step.

Knowing how to register as a dependent on Korea’s national health insurance — formally called 피부양자 등록신청 (Pibuyangjja Deungnok Sincheng — dependent registration application) — is one of the most time-sensitive admin tasks you’ll face after leaving a job. Most foreigners only discover this when they need a doctor. By then, the 14-day window may already be closing. If you’re also navigating the five most critical administrative steps after resigning, health insurance is the one that bites hardest if you miss it. I went through this myself — once when I lost my job, and again when my daughter was born and I needed to add her to my plan. The NHIS website is entirely in Korean, the eligibility rules are easy to get wrong, and nobody tells you about the 14-day deadline until it’s too late.

Why Your Health Insurance Ends When You Resign in Korea

Korea’s national health insurance system — run by the National Health Insurance Service (NHIS) — ties your coverage directly to your employment status. While you’re employed, your employer handles enrollment and splits the premium with you. The moment you resign, that link breaks.

Specifically, your 직장가입자 (Jikjang Gaipja — workplace subscriber) status ends on the last day of the month in which you resign, or sometimes on your actual last working day depending on your employer’s reporting. There’s no grace period built in. No letter arrives warning you. You’re simply no longer covered.

A common misconception is that you have a month or two before coverage lapses — as if your premium payments create a buffer. They don’t. Korea’s system is status-based, not payment-based. Once your employer removes you from their subscriber list, coverage stops. One urgent clinic visit after that date is entirely out of pocket.

What Dependent Status Means and Whether You Qualify

피부양자 (Pibuyangjja — dependent) status means you’re covered under another person’s NHIS plan without paying your own monthly 건강보험료 (Geongang Boheomnyo — health insurance premium). You get full NHIS coverage: hospitals, clinics, prescriptions, the works. The person whose plan covers you is called the 직장가입자, and they pay nothing extra for adding you.

To qualify as a dependent, you generally need to meet two conditions: first, the person sponsoring you must be an active workplace subscriber; second, you must have little or no independent income. The NHIS income threshold sits at roughly ₩20 million per year (~$14,800 USD) — if your income exceeds that, you’ll be pushed toward the local subscriber path instead. According to NHIS guidelines, foreigners on most visa types are eligible for dependent status, but your 외국인등록번호 (Oegukin Deungnoknbeonho — foreigner registration number, i.e. your ARC number) is mandatory for any application.

One more thing worth knowing: if you arrived in Korea less than nine months ago and haven’t yet built a residency record here, there’s an additional eligibility check the system runs. I noticed this personally when adding my daughter — the portal specifically flags the residency period.

Who Can Register You as a Dependent

Not every family member qualifies as a sponsor. The table below lays out exactly which relationships work, what conditions apply, and what income limits you need to stay under.

| Sponsor Relationship | Korean Term | They Must Be | You Must Be | Income Limit for You |

|---|---|---|---|---|

| Spouse | 배우자 (Baeuja) | Enrolled as a 직장가입자 | Legally married and registered | No independent income, or below ~₩20M/yr (~$14,800) |

| Parent (of the subscriber) | 부모 (Bumo) | Enrolled as a 직장가입자 | Their child — biological or legal | No independent income, or below threshold |

| Parent-in-law | 장인/장모 or 시부모 | Enrolled as a 직장가입자 | Married to their child | No independent income, or below threshold |

| Adult Child of subscriber | 자녀 (Janyeo) | Enrolled as a 직장가입자 | Under 30, or disabled/student | No independent income, or below threshold |

| Siblings / Other relatives | 형제자매 등 | Enrolled as a 직장가입자 | Living in same household and financially dependent | Strict — very low or no income |

Key insight: A spouse with active workplace insurance is by far the most straightforward path. Other relationships require additional proof of financial dependency or co-habitation. If you’re registering family members and accessing government health benefits for the first time, the spouse route saves the most paperwork — and the most stress. Speaking from personal experience: I added both myself and my daughter to my wife’s plan after I left work. Two people means two separate family documents — the portal won’t accept a single combined submission.

Documents You Need to Prepare Before You Start

The single biggest cause of failed applications is starting the online form without all documents ready. The NHIS portal doesn’t save partial progress well, and document upload errors mid-session are frustrating. Collect everything first.

When I uploaded documents for two people — myself and my daughter — the system required individual family proofs for each. One submission, two documents. Don’t assume a single 가족관계증명서 covers everyone.

If this document-gathering stage feels overwhelming, JustAskJin can help you figure out exactly which documents apply to your specific situation before you start.

Decision Flowchart: Which Path Is Right for You?

Before touching the NHIS website, work out which route applies to you. This flowchart covers every realistic scenario from the moment you resign.

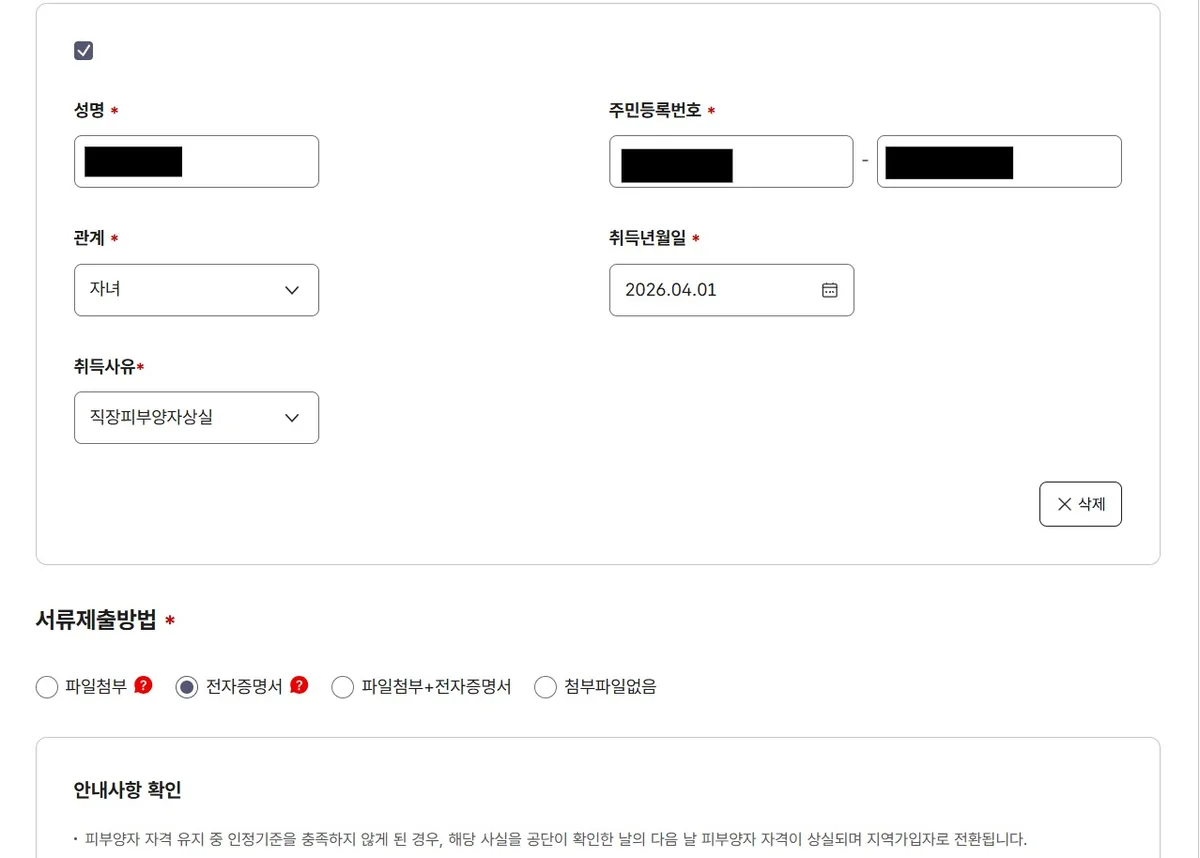

Step-by-Step: Registering on the NHIS Website

The NHIS website is entirely in Korean. That’s not a bug — it’s just reality. Here’s how to navigate it without getting lost.

Step 1 — Go to nhis.or.kr and look for the login area in the top right corner. The site renders best on desktop — mobile works but the layout shifts significantly.

Step 2 — Select the foreigner login method. You’ll see an option for 외국인 (foreigner) login, which uses your ARC number. Don’t try to use a Korean social security number here — you don’t have one. The foreigner login path typically requires your ARC number plus a phone number verification or a public authentication certificate (공동인증서).

Step 3 — Navigate to the dependent registration section. Once logged in, look for the menu section labeled 민원여기요 or similar (it translates roughly to “civil service requests here”). Under this section, find 피부양자 등록신청 (dependent registration application). The menu structure can shift with site updates — if you can’t find it, the NHIS homepage has a search bar. Type 피부양자 and select the first result.

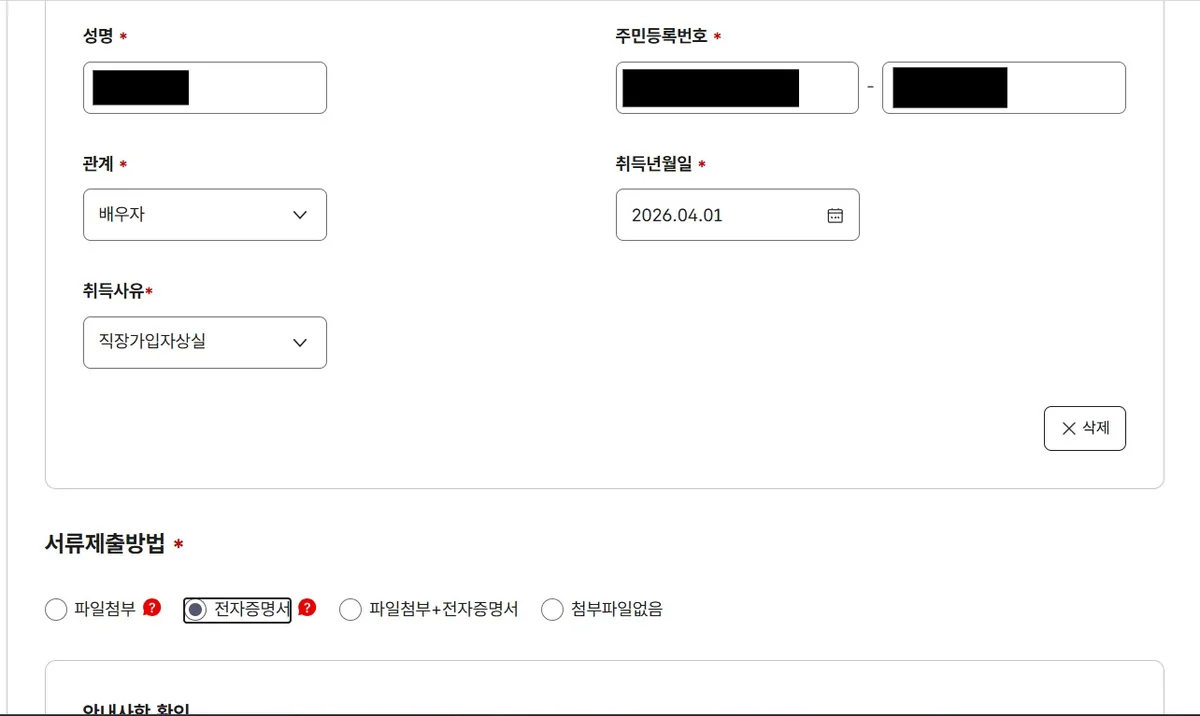

Step 4 — Fill in the dependent’s 외국인등록번호 (ARC number). This is your personal registration number. Double-check it against your physical ARC card — typos here cause automatic rejection.

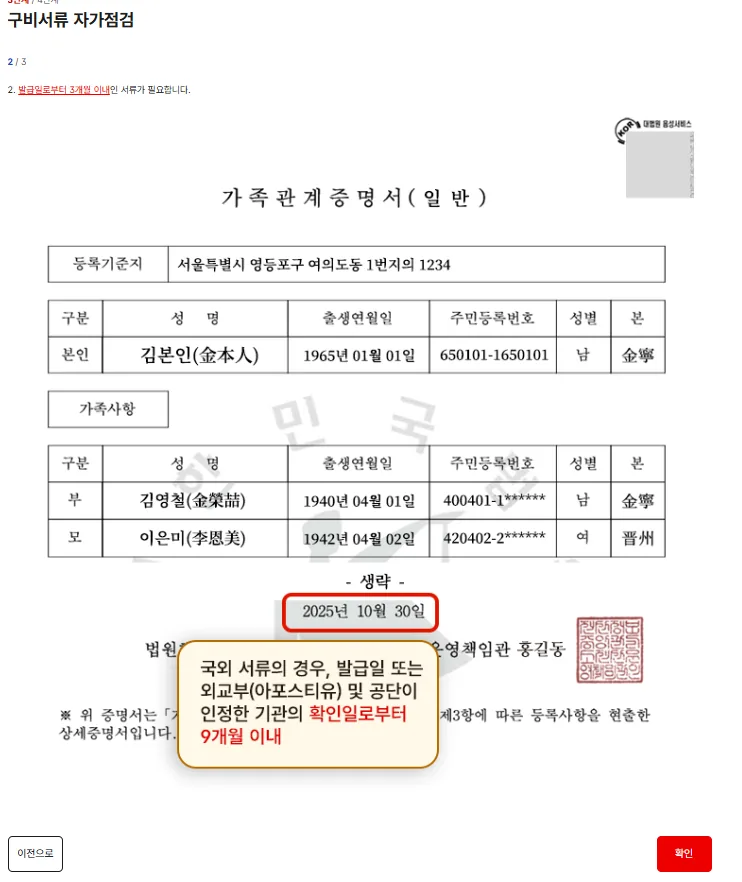

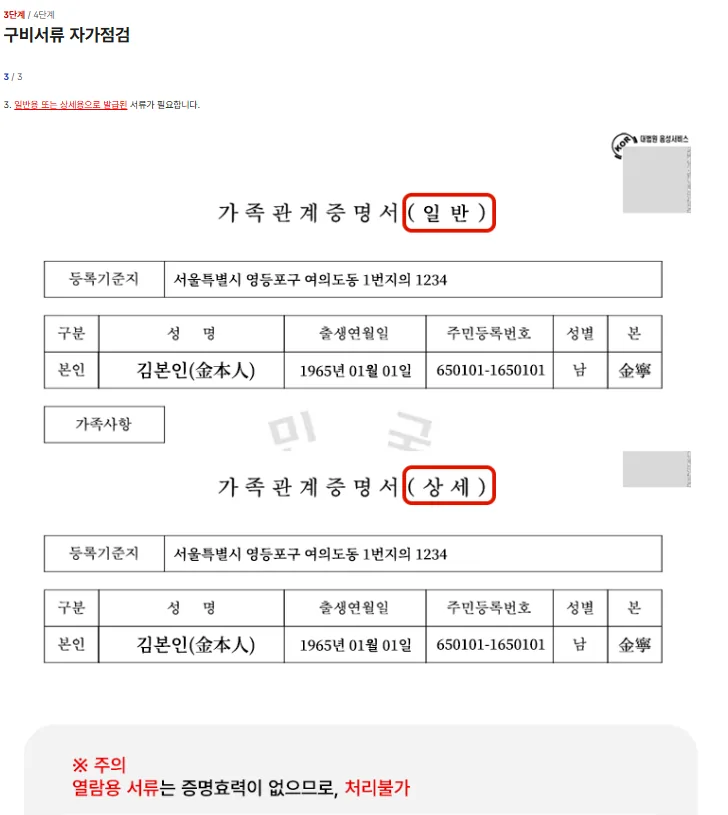

Step 5 — Upload all required documents. The portal will prompt you for each document type. When selecting document format, you’ll see options labeled 일반 (General) or 상세 (Detailed) — either is accepted for most documents.

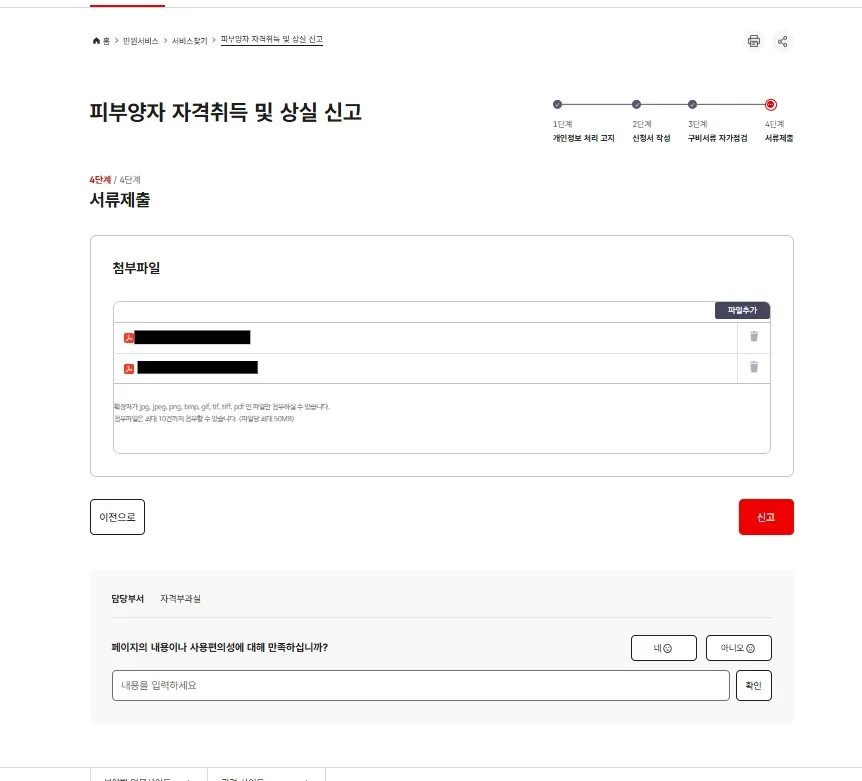

Step 6 — Submit your application. Review everything once before hitting 신청 (submit). You’ll receive a submission reference number — save it.

Step 7 — Wait for NHIS approval. Processing typically takes 3–7 business days, though straightforward cases with complete documents are often handled faster. If you submitted within 14 days of resignation, your coverage will be backdated to your resignation date. If not, coverage starts from the submission date.

Step 8 — Check your 자격확인 (Jagyeok Hwagin — eligibility confirmation) online. Log back into nhis.or.kr and navigate to your insurance status page. Once 피부양자 status is confirmed active, you’re covered.

Coverage Options Compared

Before committing to a path, here’s a clear side-by-side of your three realistic options after resigning.

| Dependent Status (피부양자) | Local Subscriber (지역가입자) | Uninsured Gap Period | |

|---|---|---|---|

| Monthly Cost | ₩0 — you pay nothing | ₩30,000–₩300,000+ (~$22–$220+) | ₩0 until you need care — then full price |

| How to Register | Family member submits form to NHIS on your behalf | Apply directly at NHIS branch or online | Nothing to register — this is what happens if you do nothing |

| Coverage Starts | From resignation date if registered within 14 days; otherwise from submission date | From the date your application is processed | No coverage — ever |

| Risk Level | Low — full NHIS coverage active | Low — full NHIS coverage active | Very high — one hospital visit can cost ₩500,000–₩5,000,000+ (~$370–$3,700+) out of pocket |

| Who This Is For | Foreigners with a spouse or household member who has workplace insurance | Foreigners with no eligible family member in Korea | Foreigners who don’t act after resigning — avoid this |

| Backdated Premiums | Possible if registered late — ask NHIS to review | Charged from the date employer coverage ended | N/A — but you pay 100% of any medical bills |

The uninsured gap is not a formal status. It’s simply what happens by default if you do nothing after resigning — and it is the most expensive outcome by a significant margin.

How to Confirm Your Coverage Is Active Online

Once NHIS processes your application, don’t assume coverage is active — verify it. You can confirm your coverage is active using the NHIS online portal by logging into nhis.or.kr with your ARC number and checking your 자격확인 (eligibility confirmation) status page. Look for 피부양자 listed next to your name. If it shows up, you’re covered. If not — or if you see 지역가입자 when you expected dependent status — call the NHIS customer service line before your next hospital visit.

The physical NHIS card is optional. Hospitals and clinics across Korea can verify your coverage in real time using your ARC number alone. You don’t need to wait for a card in the mail before seeing a doctor.

What to Do If You Have No Eligible Family Member in Korea

If no one in your household qualifies as a 직장가입자 — or if you’re living alone — dependent status isn’t an option. Your path is 지역가입자 (Jiyeok Gaipja — local/community subscriber) registration.

As a local subscriber, your 건강보험료 (health insurance premium) is calculated based on income, assets, and property — not a flat rate. For foreigners without significant Korean assets, the minimum monthly premium currently sits around ₩30,000–₩40,000 (~$22–$30), though this figure is subject to annual adjustment by the NHIS. For accurate current rates, check nhis.or.kr directly.

You can register as a local subscriber online through the NHIS website or in person at any NHIS branch office. Bring your ARC, proof of resignation, and any income documentation. Coverage typically starts from the date your application is processed.

If you have a newborn or are planning to have children soon, getting onto any form of NHIS coverage quickly matters beyond just your own health — it affects registering family members and accessing government health benefits for your child from day one.

❓ Frequently Asked Questions

How long does it take to register as a health insurance dependent in Korea after resigning?

Active effort — assuming you have all documents ready — takes roughly 60–90 minutes to complete the NHIS online application. NHIS then takes 3–7 business days to process and approve. The critical point: submit within 14 days of resignation so coverage is backdated to your last day of employment, not your submission date.

Can a foreigner register as a dependent under their Korean spouse’s health insurance?

Yes. If your spouse is enrolled as a 직장가입자 (workplace subscriber) and you meet the income threshold (roughly ₩20 million per year or less), you can register as a 피부양자. Foreign spouses need their ARC number, a marriage certificate with official Korean translation, and an income confirmation document from the National Tax Service.

What happens if I miss the 14-day dependent registration window after resigning?

Your coverage start date shifts from your resignation date to the date NHIS processes your application. Any medical costs incurred during the gap between resignation and approval date are not covered. You may also face backdated local subscriber premiums for the period you were uninsured, depending on NHIS assessment.

Does dependent status in Korea affect my visa or residency status?

Health insurance status and visa/residency status are managed by separate government bodies — NHIS for insurance, the Korea Immigration Service for visas. Registering as a dependent does not change your visa category or affect your right to remain in Korea. However, maintaining active NHIS coverage is a condition of continued legal residency for most foreigner visa types.

Do I need to register as a national health insurance dependent if I have private health insurance in Korea?

Private health insurance in Korea works as supplemental coverage — it does not replace the national NHIS plan. All legal residents of Korea, including foreigners on most visa types, are required to maintain NHIS enrollment. Registering as a dependent (피부양자) or as a local subscriber (지역가입자) is mandatory, not optional, once your employer-sponsored coverage ends.

Not sure which coverage path applies to your situation?

Visa type, income level, and family situation all affect whether dependent status or local subscriber registration is the right move. If you’re unsure where to start — or you’re stuck mid-application — JustAskJin can walk you through it in plain English.